January 2016: The Flour Report

Bias

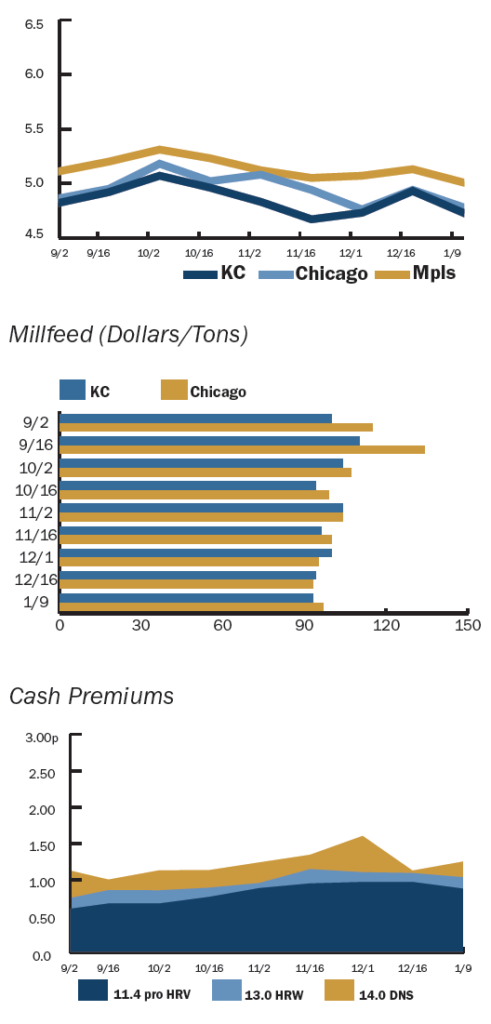

There is no compelling reason for cash premiums to do much work to get wheat moving with filled wheat bins across the plains and no urgency to move any of it due to a dearth of export opportunities. The US and Canada are residual suppliers to the world and the global glut of wheat should keep pressure on prices for the foreseeable future. The USDA report that came out yesterday reduced yields on corn and soybeans and lowered wheat acres seeded. This led to some short covering in the market that quickly settled back based on the overwhelming reality of large wheat inventories in the market. This confirms our belief that the trend should continue to be the friend of flour buyers in the coming weeks and months as there is ample moisture for planted winter wheat today.

Outside of a weather anomaly, there is very little to drive prices higher in the near term. The USDA is predicting the steepest drop in farm incomes since 1983 at roughly 28%– all driven by large grain positions across the globe depressing prices. Farmers taking a 30% hit on income will force many to reassess cash flow needs as it relates to planting intentions and capital equipment purchases where combines can run between $250-$500k each. Crop profitability decisions could lower wheat acreage even further in the spring.

Take advantage of these lows and extend coverage for 2016.

ORGANIC UPDATE

Pricing is range bound and a quiet market was seen in December with little wheat offered for sale. This should continue until spring planting season gets under way for wheat in the coming months.

BULLS & BEARS

– Winter wheat seeding report lowered acreage planted versus a year ago at 36.6 mlyn acres vs. 39.46 yr ago.

+ US exports lag 15% versus a year ago at 583 million bu for 2015-16 marketing year and carry out stocks are forecasted up 30 mil bu since December report to 941 million bushels.

FUTURES MARKET

RECAP

Weak markets in wheat continued for December. Early December saw a fugacious rally on technical short covering but that was short-lived. The Fed soon raised interest rates for the first time in almost 10 years – which added to the US dollar strength – only hurting export opportunities and putting pressure on markets further. Crop conditions for winter wheat planted were uneventful and absent any bullish inputs – pricing held in a range for much of December and as we began 2016.