December 2015: The Flour Report

Bias

An article in the NY Times posits one man’s perspective and his declaration that wheat has “terroir”; meaning it’s taste is genuinely impacted by it’s climate, soil content, and sunlight, and a return to heritage varieties and artisanal baking will shepard the industry into a new time of new products and unique tastes. Obviously, this mindset shift could lead to higher margins for the grain chain and greater awareness and larger sales for grain-based foods. Naturally, there is much interest to see this all come to fruition, however it will come down to execution, and if and when this trend can manifest itself into a real opportunity. As it will require significant collaboration and coordination vertically from the fields, to the mills, to the bakers, to the consumer. Many would love to see the de-commoditization of wheat like what coffee beans went through when Starbucks found a way to educate the masses on bean selection, leading to different taste profiles and eager customer willing to pay an up charge for the privilege to do so. That example, coupled with the renaissance for unique varieties in barley helping to drive growth and cache in the micro-brewing industry, thereby allowing farmers to contract grow for several years at agreed upon values that command a market premium. As noted above, we shall see if wheat can ever be viewed as more than a simple caloric food stuff in a packaged good form in North America and if it can become a more regional, locally sourced, higher quality and truly distinctive and desirable delectable.

Markets look to continue pattern and stay range bound over the next 30 days with basis doing much of the work if additional wheat needs to be bought. Stay out of spot market & cover Q1 2016 if you have not already done so and Happy Holidays.

ORGANIC UPDATE

Organic winter wheat offerings are tight due to reduced stocks in the US Midwest only one-third of way into marketing year, with many end-users seeking to procure year’s worth of needs early in crop year to ensure supply.

BULLS & BEARS

– USDA cut export projections to 800 myln bu from last report of 850 million bushels.

+ IGC projected global wheat stocks-to-use ratio at end of 2015-16 to 31.6% up from 29.9% a year ago.

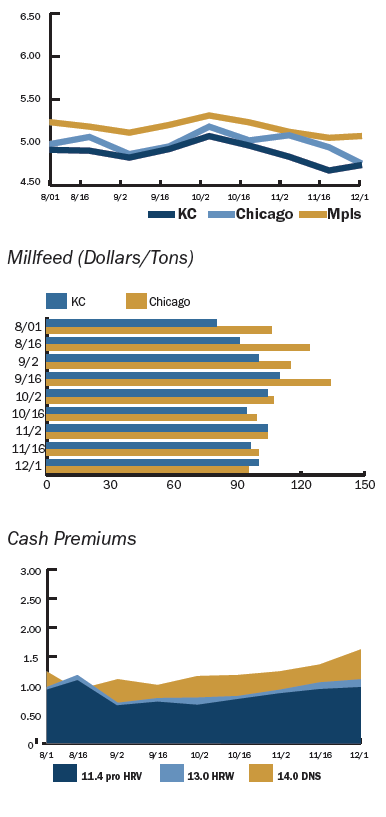

FUTURES MARKET

RECAP

Market volatility has been muted due to abundant wheat stocks and lack of fresh demand allowing wheat to slow drift lower. The USDA raised production estimates for corn, beans and raised carryout stocks on corn, beans and wheat. This coupled with a reduction in wheat export projections to lowest level since 1972 only added to the bearish tone for the past 30 days in the wheat market.